Abstract

- In bear markets or when the market is broadly expected to decline, the Long Put strategy stands out as a classic approach offering limited losses and robust downside return potential.

- Compared to directly shorting spot assets, the Long Put strategy’s key advantage is its ability to predefine maximum loss—investors only incur the cost of the options premium.

- This strategy is effective for expressing a clear bearish outlook and is also suitable for tactical risk hedging within portfolios holding long positions.

- The Long Put strategy is not merely a “directional bet”; its outcome depends on the magnitude of the decline, timing, and shifts in market volatility.

- In bear market conditions, this strategy performs best during periods where “prices are expected to fall rapidly,” rather than blindly chasing shorts when volatility is high and option premiums are expensive.

Introduction

In bear markets, investors often confront a practical dilemma: If you anticipate further market declines, what’s the best way to participate in the downward trend?

The most straightforward methods include selling spot holdings or shorting via margin borrowing and perpetual futures. However, these approaches typically involve higher capital requirements, more complex risk management, and the theoretical risk of “unlimited loss.” For those unwilling to take on extreme tail risks, while shorting offers directional clarity, it may not be the most practical strategy for sustained execution.

This is where put options become essential. Buying a put option essentially means exchanging a fixed cost for the right to sell an asset at an agreed price within a specified period. Investors have no obligation to exercise, but when the market genuinely declines, this right gains value.

The core of the Long Put strategy is “using limited cost to capture downside return flexibility.” It offers both offensive potential—profits can scale quickly when the market drops sharply—and defensive protection—if your judgment is incorrect, maximum loss is capped at the initial premium.

Long Put Strategy

2.1 Strategy Characteristics

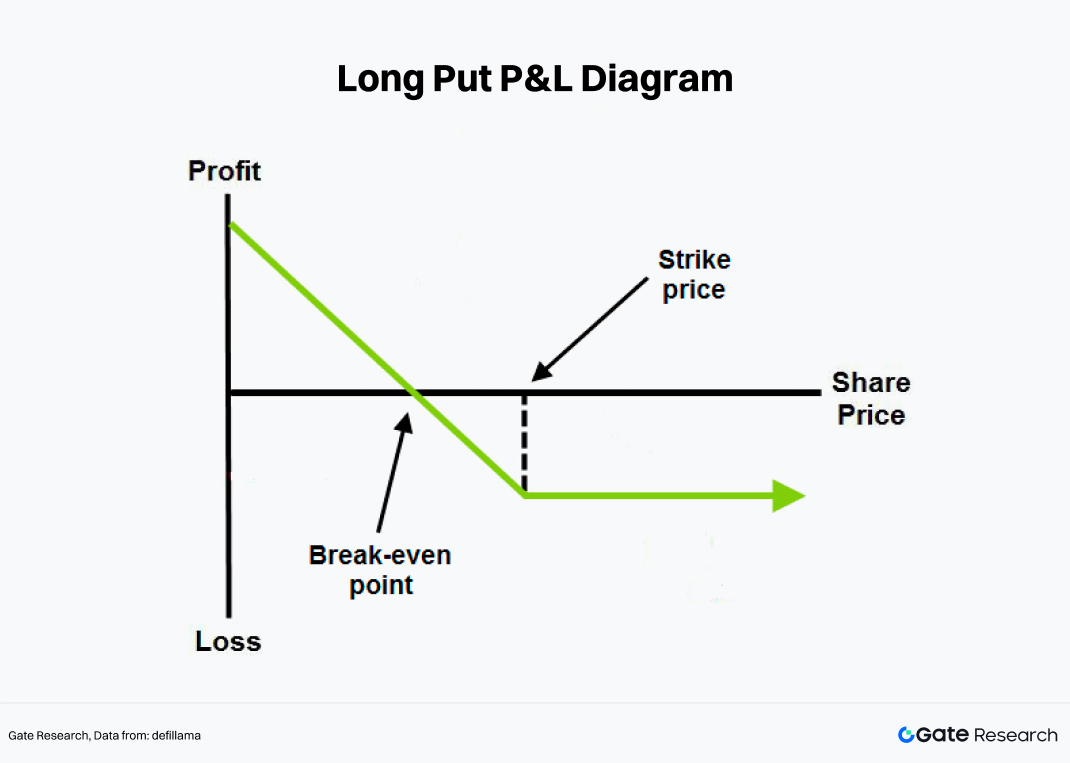

A Put Option gives the buyer the right to sell the underlying asset at the strike price on or before the expiration date. Buying a put option is commonly known as the Long Put strategy.

This strategy is best suited for investors with a clear expectation that the underlying asset will decline, ideally within a defined timeframe. Unlike spot trading, options have an expiration date. When purchasing options, investors pay a premium, essentially “buying time-limited insurance” for their market view. If the underlying price moves favorably within the option’s validity period, this “insurance” appreciates; if the market does not decline as expected or moves too slowly, the option’s time value decays and may eventually expire worthless.

From a return structure perspective, the Long Put strategy exhibits several distinct features:

- Maximum loss is limited. Regardless of how much the underlying price rises, the buyer’s maximum loss is the premium paid for the option.

- Significant downside return potential. As long as the underlying price continues to fall, the value of the put option rises, with theoretically unlimited maximum return.

- Clear breakeven point. Only when the underlying price falls below “strike price minus premium” at expiration does the trade yield a positive return.

- Highly time-sensitive. Correct directional judgment alone is insufficient; the price must decline effectively before the option expires.

Thus, while Long Put is a bearish strategy, it is not simply “useful whenever you’re bearish”; it requires a nuanced judgment of future price direction, timing, and volatility.

2.2 Strategy Advantages

Bear markets are characterized not only by price declines, but also by valuation compression, shrinking liquidity, reduced risk appetite, and heightened volatility. In these conditions, the Long Put strategy is regarded as a classic bear market tool for three main reasons:

First, it enhances the efficiency of expressing bearish views. Directly shorting the underlying asset typically yields profits proportional to the price decline; after buying a put option, during periods of accelerated decline and rising volatility, option values often show greater flexibility.

Second, it limits losses in worst-case scenarios. In bear markets, it’s common for the overall trend to weaken but for sharp rebounds to occur. Many direct short trades fail not due to incorrect directional calls, but because they cannot withstand large interim fluctuations. The Long Put’s advantage is that, even if the market rebounds abruptly, buyers won’t face unlimited losses like leveraged short sellers.

From a trading perspective, Long Put is not most effective after the market has collapsed; rather, it offers better cost-effectiveness when the “trend is just beginning to weaken and panic has not fully set in.” Once panic peaks, implied volatility—and thus option premiums—rise sharply, making puts expensive and less cost-effective.

2.3 Strategy Example

Gate currently supports bearish options trading for a range of mainstream tokens. Using BTC as an example, suppose BTC is quoted at 84,000 USDT. An investor expects that, within the next month—due to weakening macro expectations, inflows of hedging capital, and profit-taking pressure at high levels—the market may enter a further downward phase. The investor opts not to short perpetual futures but instead purchases a BTC put option with a maturity date one month out, a strike price of 80,000 USDT, and a premium of 4,000 USDT.

Key data for this trade:

- Underlying Price: 84,000 USDT

- Strike Price: 80,000 USDT

- Premium: 4,000 USDT

- Expiration Date: 30 days

- Breakeven Point: 76,000 USDT

In other words, only if BTC falls below 76,000 USDT at expiration will this trade generate a net profit.

If BTC drops to 70,000 USDT after one month, the option’s intrinsic value is:

80,000-70,000=10,000

After deducting the initial premium of 4,000 USDT, the net profit is:

10,000-4,000=6,000

Conversely, if BTC remains above 80,000 USDT at expiration, the put option has no exercise value, and the investor’s maximum loss is the initial premium of 4,000 USDT.

Long Put Strategy: Returns, Risks, and Key Variables

To fully understand this strategy, it’s not enough to remember “puts profit from declines”—you must grasp why it can be profitable and under what circumstances it may fail.

3.1 Sources of Return: Price Decline

The most direct source of return for the Long Put strategy is a decline in the price of the underlying asset. Suppose an asset is currently priced at $36.25. An investor buys a put option with a strike price of $35, a premium of $2, and 90 days to expiration. The breakeven point for this trade is $33:

35-2=33

If the price drops to $30 at expiration, the option’s intrinsic value is $5. After deducting the initial $2 premium, the net profit is $3. If the price at expiration is higher than or equal to $35, the option has no intrinsic value, and the maximum loss is the initial $2 premium paid. This is the core structure of the Long Put strategy: losses are capped when prices rise, and profits can expand as prices fall.

3.2 Time Decay: Correct Direction Isn’t Always Profitable

The biggest difference between options and spot assets is the “time” dimension.

For buyers of put options, time is often not an ally. If the market doesn’t decline rapidly as anticipated, the option’s time value erodes continuously. Even if your directional call is ultimately correct, if the drop happens too slowly or too late, the outcome may be less favorable.

This means the Long Put strategy requires not only a judgment of “will the market fall,” but also “when will it fall.”

3.3 Volatility Changes: Another Bear Market Impact

Beyond price and time, volatility is a critical variable in options trading.

Typically, the more panicked the market, the higher the option prices—especially for puts. In downturns, investors are more willing to pay premiums for protection or speculation. As a result, Long Put often benefits from rising implied volatility. However, this presents another challenge: if you buy puts after the market has already dropped sharply and panic is high, option prices are elevated. Even if your directional call is correct, a drop in volatility may offset some profits. In other words, Long Put not only bets on price declines, but also, to some extent, bets that “the decline isn’t fully priced in yet.”

Conclusion

The Long Put strategy is one of the most classic directional options strategies for bear markets. Its appeal lies in trading limited losses for powerful downside return flexibility. Compared to direct shorting, it offers superior tail risk control; compared to simply selling spot, it’s more aggressive.

However, it’s not a tool that guarantees easy profits just because you’re bearish. The challenge with Long Put is that it requires investors to make judgments on direction, timing, holding period, and volatility. If the market doesn’t decline fast or deep enough—or you enter when sentiment is extremely pessimistic—the actual results may fall short.

As a high-volatility asset, cryptocurrency provides a natural fit for the Long Put strategy. Once the market enters a phase of declining risk appetite, weakening price trends, and event-driven volatility, buying put options often becomes a strategy with both defensive and offensive attributes. Fundamentally, though, it’s not a “copy trading tool,” but a disciplined, timing-sensitive trading method.

References