The recent developments in the US-Iran conflict over the past week are continuously escalating.

The U.S. 82nd Airborne Division has canceled the “Joint Readiness Training Center” rotations, the normally sea-freighted 82nd Combat Aviation Brigade is being airlifted, and blood reserves at U.S. military bases in the Middle East have increased by 500%. The largest overseas hospital of the U.S. Department of Defense—the Landstuhl Medical Center in Germany—has suspended some civilian services.

The last time this combination of actions occurred was just before the U.S. invasion of Iraq in 2003.

In this atmosphere of heightened tension, Trump suddenly posted that there had been “very, very good and productive dialogue” between the U.S. and Iran, announcing that the U.S. would pause military strikes on Iranian energy infrastructure for five days. In the early hours of March 27, Trump posted again, extending the pause in strikes to April 6.

The stark contrast between this objective reality and Trump’s statements adds considerable difficulty to the analysis of the situation.

But beyond these public declarations, there is another channel of information known as “prediction markets,” which attempts to transform the flow of funds into interpretations of event developments, providing the world with a new perspective for information analysis.

In recent days, this money has begun to concentrate in the same direction.

Multiple insider accounts “aligning” for an imminent ceasefire

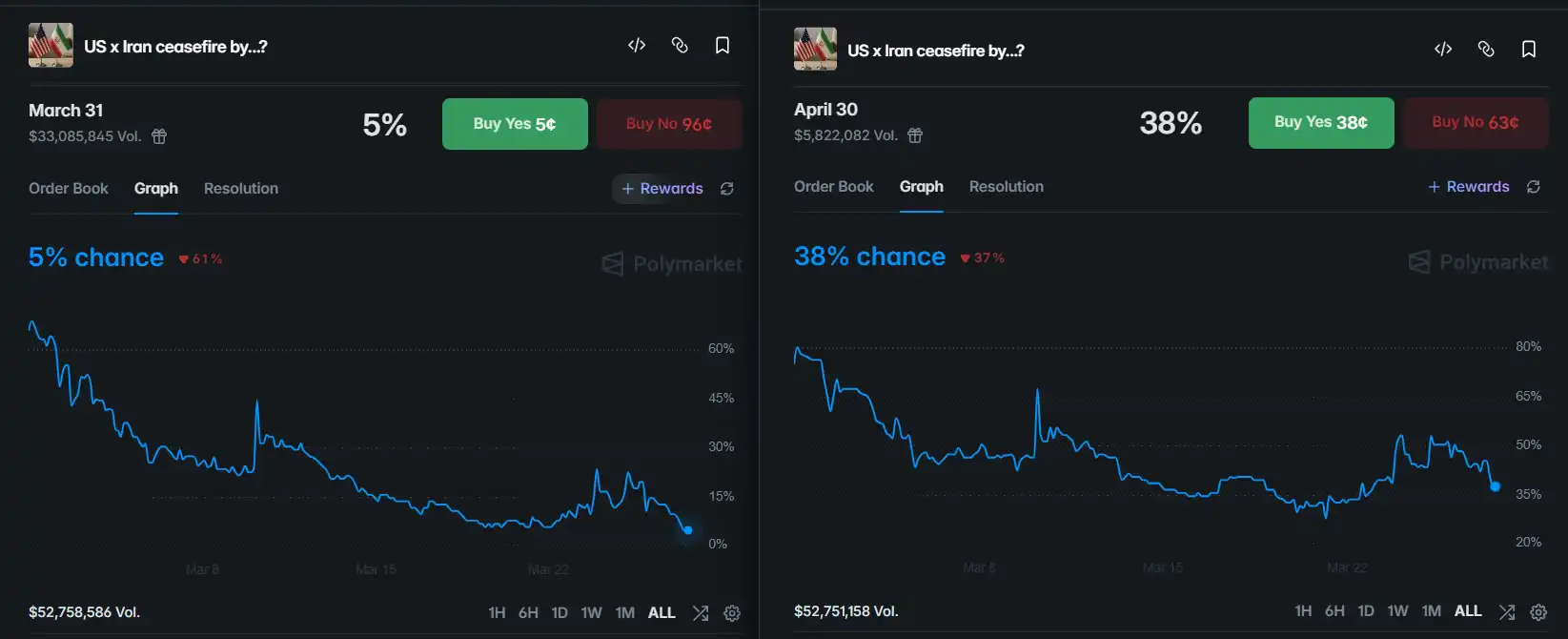

There is a trading event in the prediction market that was created only three weeks ago, with a trading volume exceeding $50 million: “Will the U.S. and Iran cease hostilities before ___ month ___ day?” If two people with differing views on this market can reach an agreement on “probability,” it will create matched trades and the corresponding likelihood of the event occurring.

The market has a very clear definition of “ceasefire”: both sides publicly announce a halt to direct military engagement. Given the escalating conflict described earlier, most people would think that in light of all the signs of military escalation, a ceasefire is a small probability event with little hope.

Just as the public thinks, the probability of a ceasefire before April 30 is about 38%, while the probability of a ceasefire before March 31 is only 5%. Many even believe that this probability should be lower—those who “overestimate” the chances of a ceasefire are likely just gamblers trying their luck without even looking at the recent news headlines.

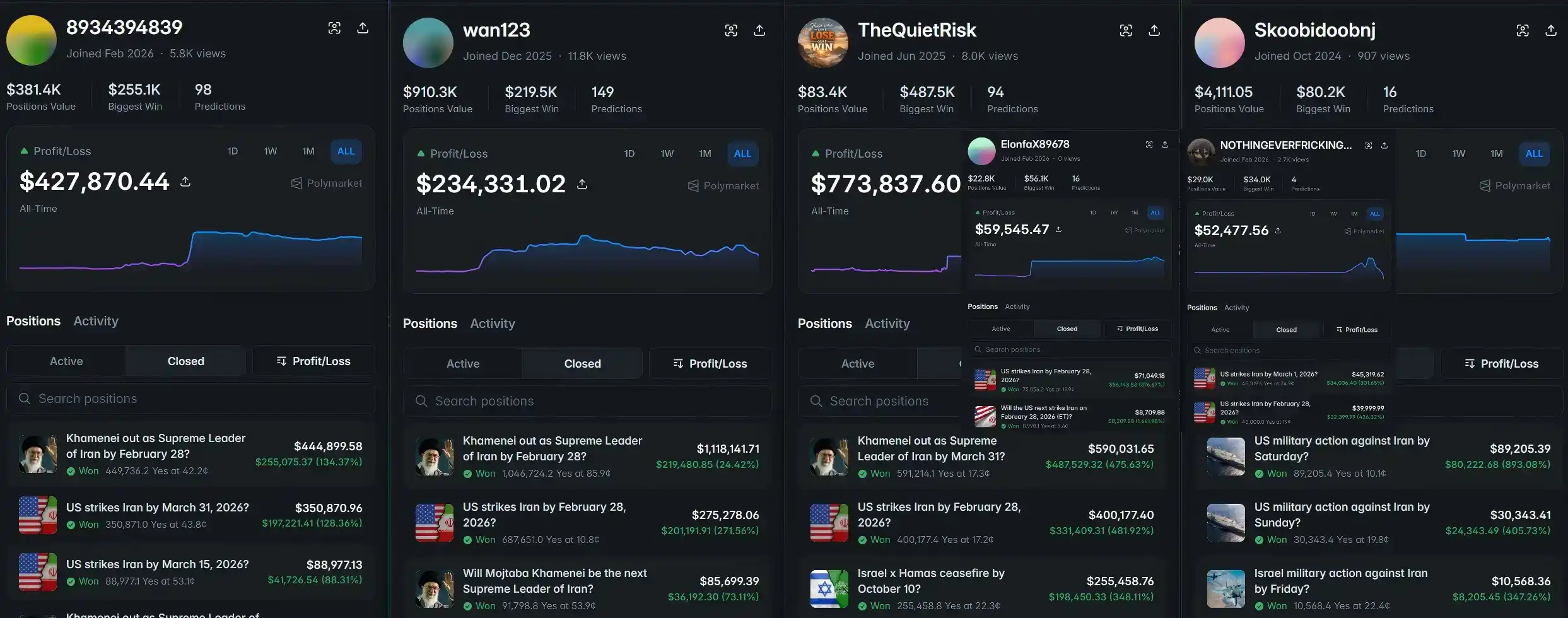

However, among these “gamblers,” six accounts have emerged that appear highly suspicious. Their total profit of $1.8 million comes entirely from accurately predicting the timing of “U.S.-Israel strikes on Iran” and “Israel-Hamas ceasefire” during 2025, as well as the outbreak of the current conflict and the assassination of Iran’s former Supreme Leader Khamenei.

This series of seemingly serendipitous predictions is not their only commonality. As of March 27, they had cumulatively invested $285,000, confidently assuming that the U.S. and Iran would reach a ceasefire before April 30, with $185,000 of that in the market for “U.S.-Iran ceasefire before March 31.”

If these six accounts can truly “foresee the future,” then we can reverse engineer their positions by using “knowing in advance that there would be a ceasefire” to deduce their stances.

Why Iran would want a ceasefire

This might be the moment when Iran is in the strongest negotiating position with the most leverage in this war: the blockade of Hormuz has driven up global oil prices, no other countries are directly involved in the strikes apart from the U.S. and Israel, and the narrative of resistance and patriotism brought by the new leadership has gathered public support.

Conversely, if the fighting continues, the gradual shift of pro-U.S. Gulf states like Saudi Arabia and the UAE, the continued depletion of Iran’s military capabilities, and the development of alternative shipping routes through Hormuz will all lead to Iran losing its dominant position at the negotiating table.

At this point, it is necessary to mention a very sharp question: on the eve of this war, the U.S. and Iran were negotiating in Geneva, and the progress at that time was described by all parties as “productive,” even “a historic agreement was within reach.”

However, the U.S. and Israel launched a sudden attack on Iran while negotiations were still ongoing. With this precedent, how can Iran trust that the U.S. will honor a ceasefire commitment?

This brings us to the nature of the ceasefire itself: for Iran, the ceasefire is not a trust issue but a matter of calculating interests. If the agreement is reached and the U.S. tears it up again, Iran will further solidify the narrative of “the U.S. being untrustworthy” on the international stage; if the agreement is upheld, Iran locks in the most favorable negotiating outcome currently available.

This also explains why, although Iran publicly stated “no negotiations,” it has maintained information flow through multiple intermediary channels and specifically proposed counter-proposals. The public statements are performances for the domestic audience, while actual contacts are aimed at securing the best exit conditions.

Additionally, Iran’s network of proxies has suffered from organizational fractures, ammunition depletion, and other issues in this round of conflict. Coupled with its domestic economy being on the brink of collapse even before the war (the Iranian rial has depreciated nearly 90% compared to 2018), taking a favorable exit may be their optimal solution.

The U.S., the farthest from the battlefield, wants a ceasefire the most

Nearly a month into the war, the S&P 500 index has fallen continuously from pre-war levels, with the Dow Jones having recorded four consecutive weeks of losses, setting a three-year record for the longest losing streak; gasoline prices have soared from $2.98 before the war to $3.98, rising over 30% in three weeks; the 30-year fixed mortgage rate has increased by half a percentage point; Goldman Sachs has raised the probability of recession to 30%.

These core data have limited short-term impact on the average American, but they are fatal for Trump—stock market performance and WTI oil prices are core indicators of his administration’s success.

The most ideal tool for the U.S. government at this time—the Strategic Petroleum Reserve—has seen its effectiveness significantly reduced due to aging facilities. Since this system, built after the 1975 oil crisis, has a design life of only 25 years, its actual sustainable release capacity may be only half of what is officially advertised, or even lower.

More critically, extracting crude oil further dissolves the internal structure of the salt caverns, meaning that large-scale releases will also accelerate system aging. Using this release as a narrative tool can indeed help Trump stabilize market sentiment in the short term; however, if the conflict drags on, the drawbacks of this countermeasure may manifest in the form of surging oil prices on the candlestick charts.

In addition to financial data, domestic politics in the U.S. are also a factor that Trump must weigh in this round of conflict. When the Iraq War broke out, George W. Bush’s approval rating was as high as 72%; when the Afghanistan War began, his approval rating exceeded 90%.

However, on the first day of this war, Trump’s approval rating was below 40%. Even the classic “rally-around-the-flag effect” in political science—where a president’s approval rating rebounds due to the outbreak of war—did not occur in this round of strikes. As of March 25, Trump’s overall approval rating had dropped to 36%, setting a new low for his second term.

Moreover, coupled with his campaign promise of “No New Wars,” Trump’s current performance on the American political stage not only jeopardizes the prospects of his core circle in the midterm elections later this year but also undermines the entire Republican camp’s voice in the 2028 presidential election.

On the other hand, Trump has also set a hard deadline of May 14 for himself. Due to the need to “stay in Washington to handle the current combat actions,” he postponed his originally planned trip to China next week and publicly announced yesterday that the schedule would be extended to May 14.

Everything is changing, but TACO will not change

There is currently a term specifically describing Trump’s sudden announcement of positive developments after extreme pressure: TACO. It stands for Trump Always Chickens Out.

However, in such a tense geopolitical situation in the Middle East right now, many believe he will not TACO, let alone successfully convince Iran to agree to a ceasefire.

Three months ago, if someone had told you that Trump would bring Venezuelan President Maduro back to a U.S. court like catching a chick, threaten European allies with Greenland as a tariff bargaining chip at the Davos World Economic Forum, and kill their highest leader during negotiations with Iran—

These events, which were previously thought to have less than a 1% probability, have all happened. And now what we are watching for in the future is whether the extremely low probability of a U.S.-Iran ceasefire TACO will play out as expected in the coming month.

Click to learn about job openings at BlockBeats.

Welcome to join the official community of BlockBeats:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Twitter Official Account: https://twitter.com/BlockBeatsAsia