AI agents have sparked apocalyptic talk about SaaS, but the scarcity has shifted toward proprietary data and business context—whoever controls the data will be the rent collector of the next decade.

After AI agents took off, many people have already started writing eulogies for SaaS. But I think it’s still too early.

Investors really are panicking. In early 2026, the panic over the SaaS doomsday swept across the entire tech industry. By the end of January, after Anthropic released just a feature update enabling Claude to call extension applications, the U.S. software sector’s market value then evaporated by thousands of billions of dollars over the next three weeks.

Their logic is pretty straightforward. They think that since AI can already write code on its own, find bugs, and even dynamically generate tools, the cost of writing code is getting infinitely close to zero. Once an agent can create all kinds of custom tools for enterprises anytime and anywhere, those software companies that charge monthly rent will naturally lose their moats overnight.

So from CrowdStrike to IBM, from Salesforce to ServiceNow—no matter how bright the earnings reports look, they’re all going through brutal sell-offs.

At the same time, countless AI founders are holding BP and telling VCs they want to “build the middle layer of the Agent era,” or “For Agent startups.”

They’re all betting on one thing: building tools is the sexiest business in this era.

But if we pull our eyes away from those PPTs and look at the real workings of businesses, you’ll find it’s actually not like that at all.

Software isn’t sold as code

In economics, there’s a classic theory that’s been repeatedly validated, called “the transfer of factor scarcity.” Each productivity revolution makes some previously scarce inputs abundant, while making another previously ignored input extremely scarce, and wealth then concentrates on the latter.

Before the Industrial Revolution, labor was scarce; steam engines made mechanical labor abundant, so scarcity shifted to capital and factories—meaning factory owners became the richest people of that era.

The internet revolution made the cost of information transmission effectively zero, so scarcity shifted to users’ “attention,” and traffic became a huge business.

Now, the AI revolution is making the ability to write code and build tools extremely abundant. In the Agent era, where code is no longer scarce, where does scarcity shift to?

In fact, over the decades of software industry development, code itself has never truly become a moat.

Every line of code in the Linux system is free, but that doesn’t stop Red Hat from being acquired by IBM for a staggering $34 billion. MySQL is free; after Oracle brings it into its portfolio, it can still sell expensive service contracts based on it. Anyone can download PostgreSQL’s code, but AWS Aurora’s database service still pulls in billions of dollars per year from enterprise customers.

When code becomes free, the business is still there—and it’s doing quite well.

The key is really these three things: business processes that have been hardened over time, customer data that’s been accumulating for years, and the extremely high switching costs generated by that.

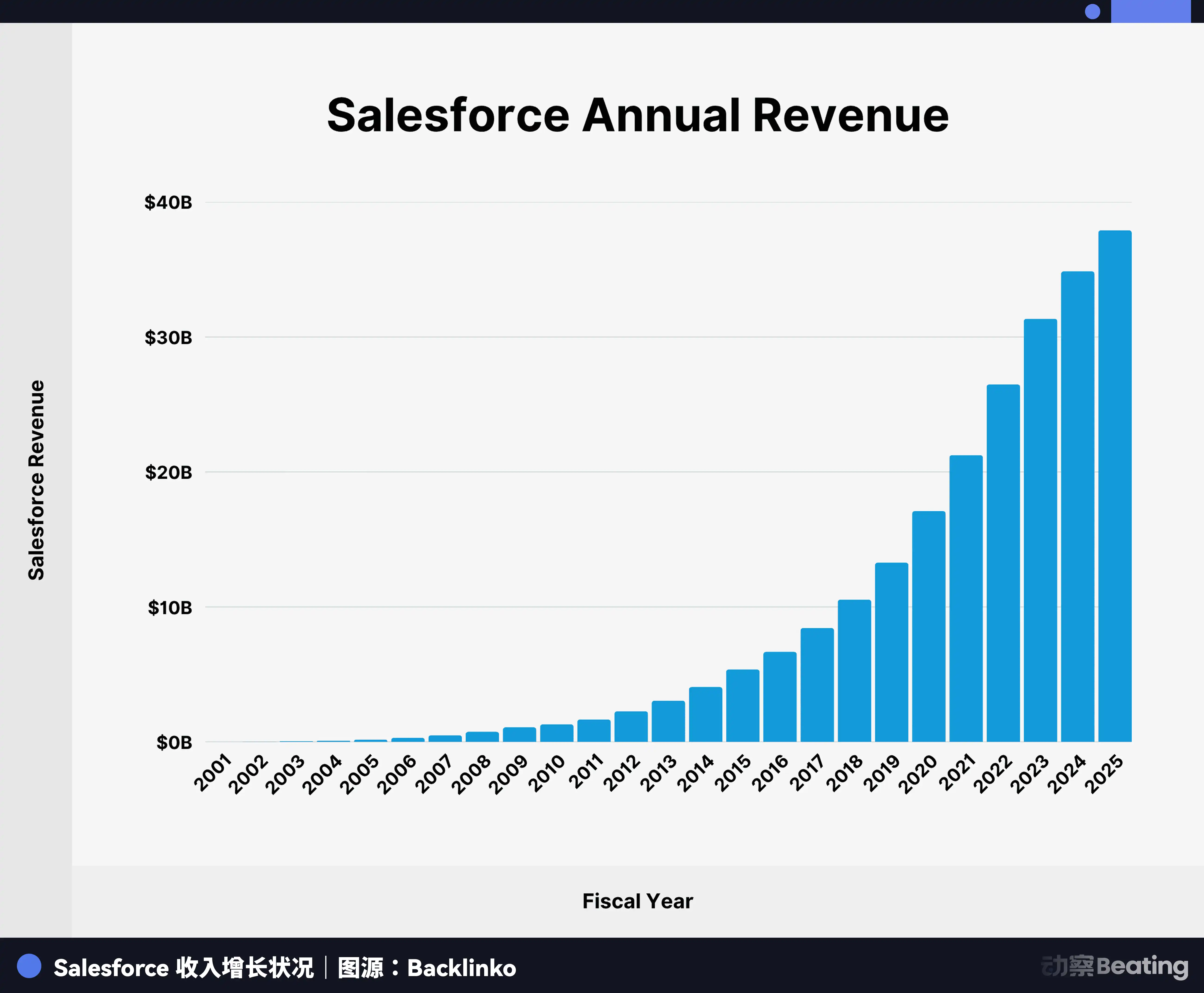

When you buy Salesforce, you’re not buying the source code of that CRM system—you’re buying the more than 500 billion records of enterprise customers behind it, and the process experience that tightly interlocks sales, customer service, marketing, and so on. Those data aren’t cold, line-by-line code; they’re living time and history from the enterprise.

A company has been using Salesforce for ten years, and every customer communication record, every transaction history entry, and every follow-up node in each sales opportunity is all in there. If you want to move away, it’s not just a matter of switching software—it’s essentially relocating the company’s entire memory. That’s why Salesforce can still deliver $41 billion in annual revenue and set its 2030 target at $63 billion.

Image source: Backlinko

Back in the framework of the transfer of factor scarcity: since an agent can create tools on its own and the cost of writing code has gone to zero, what is actually the scarcest factor in the context of enterprise services?

Choking the Agent’s “throat”

What truly keeps an agent from functioning isn’t that it doesn’t have hands—it’s that it doesn’t have the “context” in its head.

A super agent with all the tools is like a top-performance juicer. It spins extremely fast and has razor-sharp blades, but if no one puts fruit into it, it definitely can’t produce a cup of juice for you.

In its annual report, McKinsey pointed out that 88% of enterprises are using AI, but only 23% have actually achieved scalable deployment of agent systems in some part of their organization. What holds them back isn’t that the big models aren’t smart enough—it’s that the company’s data architecture hasn’t been prepared.

In an interview with MIT Technology Review, SAP’s president of data and analytics, Irfan Khan, said: “A company can’t just throw out its entire general ledger system and replace it with an agent, because an agent can do nothing if it lacks business context.”

By “business context,” we mean: where the company’s financial compliance bottom line is; what regulatory requirements exist in this industry; the preferences and history of this customer over the past decade; the vendor’s payment terms and records of defaults; the employee’s performance history and promotion paths… these things are neither publicly available online nor retrievable through crawling—and they also can’t be predicted and generated by AI via text.

Foundation Capital partner Ashu Garg also shares the same view. He said that what an agent needs isn’t just data, but a “context knowledge map”—an inferencing layer that can capture not only what an enterprise has done, but also how the enterprise thinks. This kind of thing can only be distilled from real business operations; it can’t be manufactured out of thin air.

Under this logic, scarcity has shifted from “the ability to build tools” to “owning irreplaceable business-context data.”

If the agent can’t make a cup of juice on its own, then where exactly are those fruits in the end?

The golden age of data landlords

The answer points to those old players that were once thought to be doomed by AI.

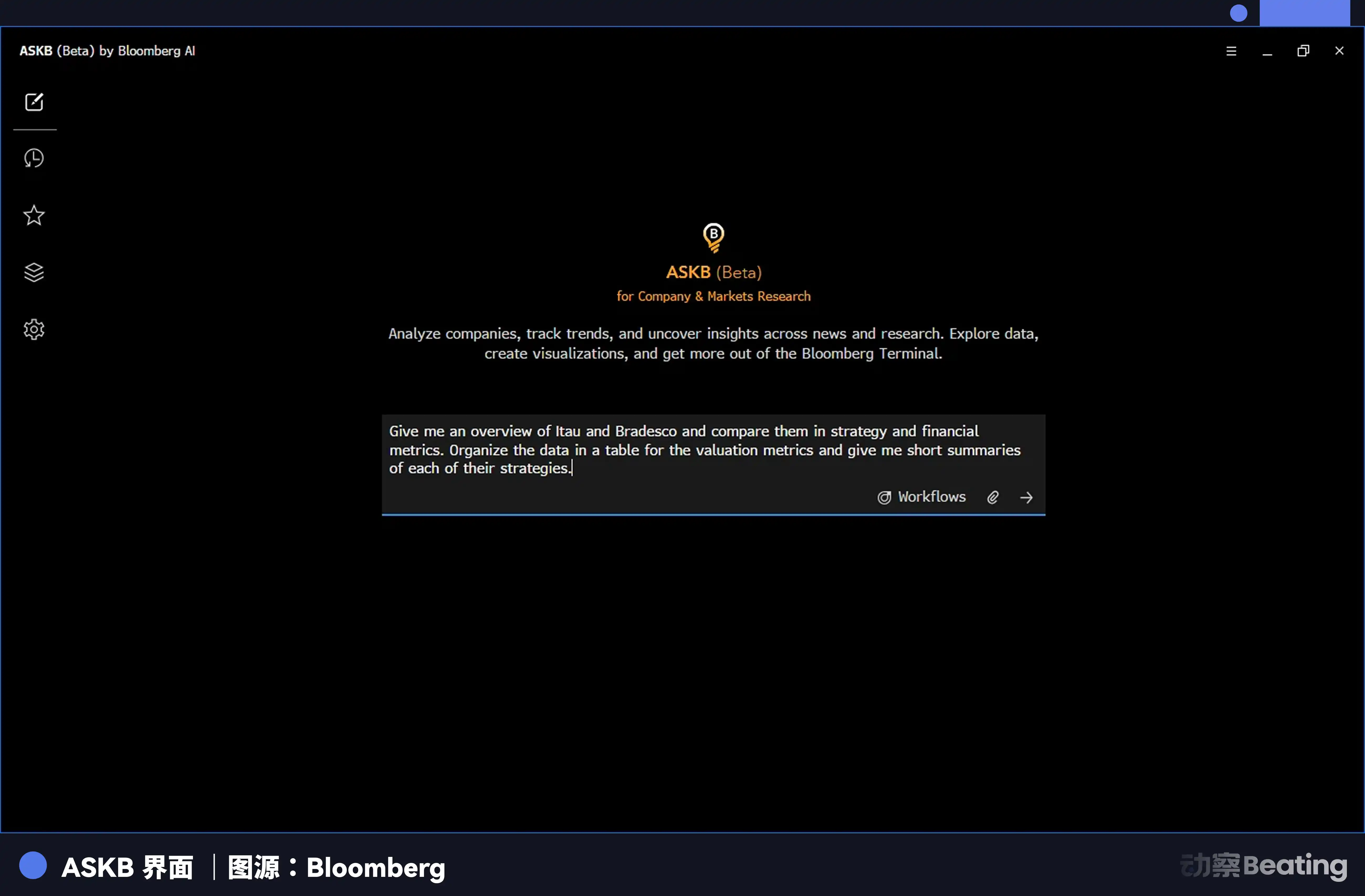

On February 23, 2026, Bloomberg launched an agentic AI interface called “ASKB.” Bloomberg Terminal is one of the most representative products in the software industry. Although there are only 325,000 subscription users worldwide, each account costs $32,000 per year. That means Bloomberg can collect more than $10 billion in annual revenue from just those 325,000 accounts, accounting for over 85% of Bloomberg LP’s total revenue.

Image source: Bloomberg

For internet industries that believe “more users is better,” this is actually counterintuitive. Bloomberg has built a solid business fortress on the backs of a tiny number of paying users.

The reason it’s able to do this is simple: Bloomberg possesses the most complete, most timely, and most deeply structured financial data in the world. These data are the product of decades of continuous investment, including real-time quotes, historical archives, news corpora, analyst reports, and company financial data. Any organization that wants to make serious decisions in finance can’t do without it.

For the newly launched ASKB, AI is the engine, and Bloomberg’s proprietary data is the only fuel. Any agent that wants to play a role in the financial industry can’t fabricate these data out of thin air—it can only obediently connect to Bloomberg’s interfaces.

WatersTechnology offered a very sharp commentary: Bloomberg’s agentic positioning shows “how those who have data turn AI into their own cash machine.”

This logic holds across all vertical industries as well. Veeva controls compliance and R&D data for the global pharmaceutical industry. Any pharmaceutical company’s agent must call those data to handle clinical trials and regulatory filings. Epic controls medical health records for more than 250 million patients in the U.S., and every diagnostic recommendation by a healthcare agent needs real patient record data as its foundation. LexisNexis monopolizes massive legal document archives, and when legal agents need to perform case retrieval and compliance analysis, they can’t get around it.

These data are the crystallization of decades of business operations in the real world—time distilled, a history that can’t be copied. This is the ultimate manifestation of “the transfer of factor scarcity”: when everyone has top-tier AI engines, what truly decides outcomes is whether you can find the oil field that’s unique to you.

In the past, these subscription data services were sold to human analysts. A large organization might need to buy 100 Bloomberg Terminal accounts. But in the future, when machines become consumers of data, it could be a single organization operating tens of thousands of agents, which in milliseconds will go all-out calling those proprietary data interfaces.

This is a leap in magnitude. The number of queries a human analyst can handle in a day is limited, but an agent’s calling frequency can be orders of magnitude higher than a human’s. The demand for continuous, real-time, high-value data will see an exponential surge. The subscription business logic won’t be overturned—if anything, it will be amplified infinitely by machines’ appetite.

Code goes to zero, and data starts collecting rent.

But does that mean every SaaS and data company can rest easy?

Not all SaaS has this ace card

If you interpret this article as indiscriminate bullish hype on the SaaS industry, then you’re completely wrong. What AI brings to SaaS is a brutal wave of large-scale polarization.

In early March 2026, TechCrunch interviewed a group of digital top-tier VCs and asked what they least want to invest in right now.

Silicon Valley investors are already voting with their feet. Simple workflow packaging, horizontal tools that can be applied to any industry, lightweight project management—stories that once could carry a funding round are now sharing the same fate of being directly passed over. The reason is simple: these agents can do it all easily. Software companies without exclusive data are rapidly losing their eligibility to be seen by capital.

This judgment splits the SaaS world into two halves.

One half is tool-type products that only provide thin wrappers—put a nice interface on top of public data, or only optimize a single-point operational workflow within a SaaS. The moat of these products, in essence, is user habits and interface stickiness.

But as Jake Saper of Emergence Capital put it: “In the past, building habits for humans inside your software was a powerful moat. But if agents are doing this work, who cares about human workflows?”

These SaaS products genuinely face a serious threat. A GTM tool stack is a textbook example. Gainsight, Zendesk, Outreach, Clari, Gong—these companies each occupy neighboring functions such as customer success, customer support, sales outreach, revenue forecasting, call analytics, and more. Each requires its own budget, its own operations, and its own integrations. In AI-native companies, one agent can now connect all these steps, and the value of those point tools will be greatly diminished.

The other half of SaaS is deeply embedded in the core business processes of enterprises, and they hold non-substitutable proprietary data. These companies won’t be replaced by agents—if anything, they’ll become more valuable because of the existence of agents.

Take Salesforce as an example. In February 2026, Salesforce’s financial report showed Agentforce’s annual recurring revenue reached $800 million, up 169% year over year. It delivered a cumulative 2.4 billion “agentic work units” and processed nearly 20 trillion tokens in total. More than 29,000 Agentforce customers have been signed, up 50% quarter-over-quarter. Even more importantly, the combined ARR of Agentforce and Data 360 exceeded $2.9 billion, up more than 200% year over year.

During the earnings call, Marc Benioff said: “We’ve rebuilt Salesforce into the operating system for an Agentic Enterprise. The more AI can replace work, the more valuable Salesforce becomes.”

Salesforce hasn’t been replaced by agents—instead, it has become the soil where agents run. Its value comes precisely from the business data and process context it controls that agents can’t bypass.

ServiceNow’s CEO Bill McDermott publicly announced in February 2026: “We’re not a SaaS company.”

Image source: Business Insider

He isn’t denying it—he’s actively cutting himself. His logic is that SaaS is a concept about the “software delivery method.” What ServiceNow wants to become is the orchestration and execution layer for enterprise AI agents: AI can discover problems and provide recommendations, but the actual actions executed inside enterprise systems still require a workflow-deeply embedded platform like ServiceNow.

Workday, on March 17, 2026, released “Sana,” a conversational AI suite that deeply integrates HR and finance data. The core logic of this product isn’t to replace Workday with AI, but to feed AI with Workday’s data.

Workday holds data for thousands of enterprises on compensation, performance, organizational structures, and financial budget. The depth and uniqueness of these data are impossible for any AI-native startup to replicate in the short term.

So the real moat isn’t whether you have data—it’s whether the data in your hands is unavailable, unbuyable, and unbuildable by others.

In the next decade, who will be collecting rent

With every technological revolution, the party that ultimately captures the largest profits is often not the person who invented the earth-shaking new technology, but those who quietly secured the scarce factors that the new technology depends on. In this era of rapid AI development, large model capabilities will keep getting stronger, and the ability for agents to write code and build tools will keep becoming more widespread.

When these once-considered “black tech” capabilities become infrastructure, the logic of “the transfer of factor scarcity” boils down to one conclusion: the people who are busy building tools for agents are very likely not the winners of the final game of this era.

In its February 2026 analysis, Foundation Capital said that the total market value of the software industry will expand to 10 times what it is now over the next decade. But this 10x growth won’t be distributed evenly across all software companies—it will be highly concentrated among the players who can truly harness the Agent era.

The real winners are those who hold data assets that agents can’t bypass.

For today’s founders and investors, there are only two possible destinies in this era: one is to spend everything building shovels for agents, and the other is to grab the land first. What you’re doing right now, you should know in your