CoinShares, a research firm, published its Q1 2026 Bitcoin mining report on March 31, confirming that Q4 2025 was the toughest quarter miners have faced since the April 2024 halving. The combination of a Bitcoin pullback and record-high total network hashrate has compressed the hashrate price to roughly $28–$30 per PH per day, setting a historical low after the halving; estimates suggest that about 15–20% of the network’s older mining rigs have fallen into losses.

Severe Troubles in Mining in 2025 Q4: Five Key Core Crisis Indicators

(Source: CoinShares)

(Source: CoinShares)

CoinShares’ report notes that the deterioration in hashrate price has been worse than previously expected. In early March 2026, it briefly touched about $28 per PH per day; as of the time of writing, it has rebounded to the $30–$35 range. At this level, miners operating older-generation rigs (energy efficiency ratio of about 29.5 J/TH) are already loss-making if their electricity price is higher than $0.05 per kilowatt-hour. Meanwhile, the fourth quarter saw three consecutive mining difficulty reductions— the first time this has happened consecutively since July 2022— which, at the technical level, formally marks the “Miner Capitulation” signal.

Core Data Indicators of the Mining Crisis

Hashrate price (Hashprice): Down to as low as $28 per PH per day in March 2026, the historical low after the halving

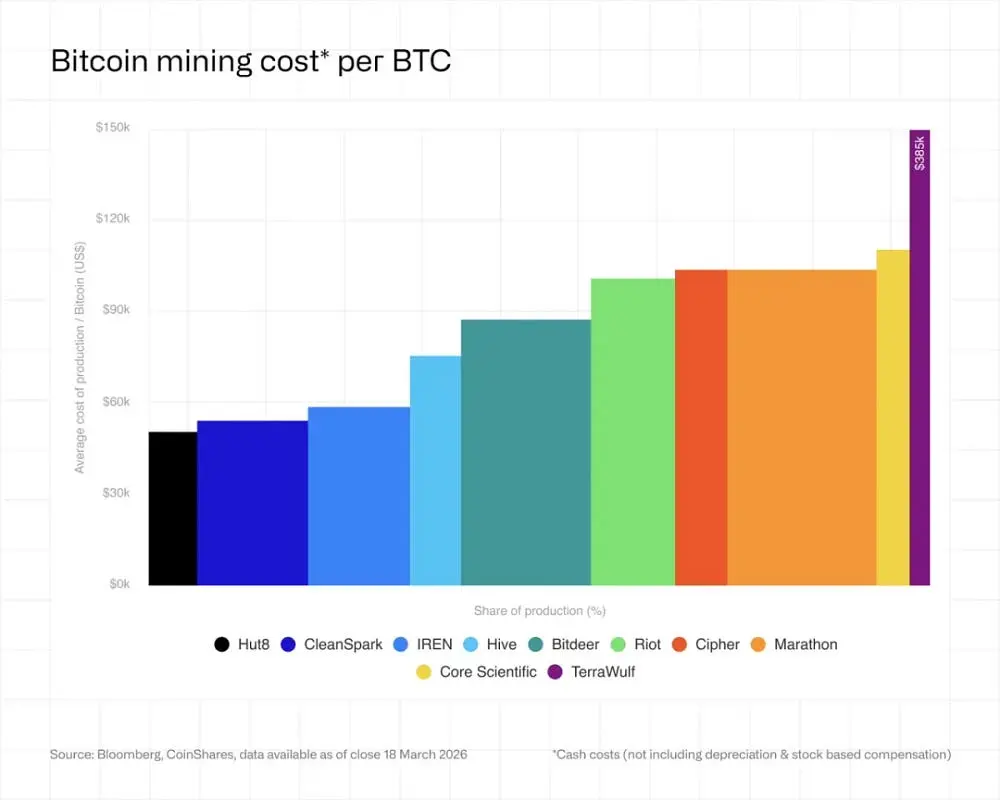

Weighted average cost: The cash cost of producing a single BTC in Q4 for publicly listed miners rose to $79,995

Loss ratio of older mining rigs: Estimates indicate that about 15–20% of equipment across the network is operating at a loss

Consecutive difficulty reductions: Three consecutive reductions in Q4, the first time since July 2022, marking miner capitulation

Network hashrate pullback: From the October peak of 1,160 EH/s, down about 10% to 1,045 EH/s by end of December

CoinShares’ forecast: If BTC rebounds to $100,000, the hashrate price could rise back to $37 per PH per day; if it challenges the $126,000 all-time high, it could spike to $59. Total network hashrate is expected to rebound to 1.8 ZH/s by the end of 2026.

AI Transformation Creates a Split: Structural Reorganization in the Mining Sector

CoinShares’ report reveals that publicly listed mining companies have cumulatively announced more than $70 billion in AI/HPC high-performance computing contracts, and mining is accelerating its split into two sharply different sub-sectors.

Infrastructure Transformation Camp: Companies such as WULF, CORZ, CIFR, and HUT are increasingly evolving into operators centered on AI data center businesses, while Bitcoin mining’s share continues to shrink. The capital markets are assigning an extremely high valuation premium to the AI narrative— mining companies that have secured HPC contracts have valuation multiples (EV/NTM sales) of 12.3x, while purely mining companies have only 5.9x.

Pure Mining Camp: Low-leverage miners such as CleanSpark (CLSK) and HIVE have demonstrated strong financial discipline. HIVE’s debt interest cost is only $320 per BTC (total debt of just $13.8 million), and CLSK’s interest cost is similarly very low ($830 per BTC). During the hashrate-fee trough, they have clear structural advantages for survival.

This split has led to a fundamental reshaping of capital structures: IREN assumes $3.7 billion in convertible notes, WULF’s total debt reaches $5.7 billion, and CIFR has issued $1.733 billion in senior secured notes. The rapid rise in overall sector leverage has fundamentally changed the risk profile of the mining sector. CoinShares forecasts that in 2026, mining sector consolidation and M&A activity will further increase, and miners with healthy balance sheets are expected to become the acquirers.

Frequently Asked Questions

What is hashrate price (Hashprice), and why does it determine miners’ survival or demise?

Hashrate price is the core metric that measures the revenue generated per unit of hashrate (per PH per day), determined jointly by three factors: the BTC market price, the network’s mining difficulty, and transaction fees. When hashrate price falls to $30 per PH per day, older rigs lagging in energy efficiency cannot turn a profit and are forced to shut down or sell equipment, leading to a “miner capitulation” phenomenon.

What exactly does “Miner Capitulation” in the CoinShares report refer to?

Miner capitulation refers to miners shutting down in large numbers or selling BTC because mining is no longer profitable. On technical indicators, three consecutive mining difficulty reductions are viewed as a capitulation signal, because a difficulty reduction implies that a large amount of hashrate has already exited the network. CoinShares data shows that the BTC treasury holdings of publicly listed miners have decreased by more than 15,000 BTC from their peak.

Is the mining AI transformation trend sustainable?

CoinShares’ analysis indicates that the current trend reflects more the relative advantage in returns between AI and mining, rather than a permanent industrial transformation. If the BTC price rebounds meaningfully, some companies may reassess the capital allocation proportions between the two types of businesses. The report believes that the group of purely mining companies may shrink, but will not disappear entirely; miners with excellent energy efficiency or access to special power resources will still have a place in the market.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.