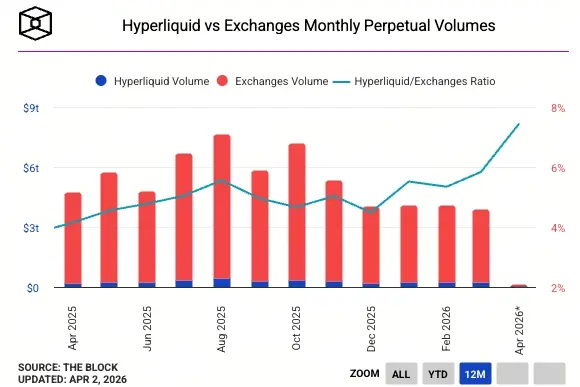

The share of the decentralized exchange Hyperliquid in the global sustainable futures market rose to nearly 6% in March, with monthly trading volume nearing $200 billion. In the same period, centralized exchanges (CEX) handled more than $3 trillion in monthly trading volume for sustainable futures, indicating that Hyperliquid’s absolute scale still remains significantly behind that of mainstream centralized platforms.

The core significance of doubling market share: a structural signal of growth against the cycle

Over the course of a year, Hyperliquid’s market share rose from 3.5% to nearly 6%. In the decentralized derivatives space, this increase implies that its relative scale has nearly doubled. The context behind this growth gives the numbers deeper meaning: while overall market trading volume is shrinking, its relative share continues to climb, showing that Hyperliquid is taking real trading activity away from competing platforms—not merely benefiting passively from market hype.

In the on-chain competitive landscape, although dYdX and GMX both provide decentralized perpetual contract services, their trajectories in trading volume growth and product expansion have not been able to match Hyperliquid’s momentum. The latter has already established a leading position in the decentralized perpetual futures arena.

Expansion beyond crypto assets: a structural competitive advantage for around-the-clock trading

(Source: The Block)

(Source: The Block)

Hyperliquid’s share growth comes not only from the accumulation of crypto-native trading volume, but also from its systematic extension into the non-crypto asset space. At present, commodities such as oil are traded around the clock (24/7) on the Hyperliquid platform, and the share of non-crypto asset trading volume in the platform’s overall activity continues to rise.

This expansion direction precisely targets a structural weakness of traditional centralized exchanges. For instance, in oil derivatives, institutional traders who use CME (Chicago Mercantile Exchange) must wait until CME opens on Sunday evening to hedge positions held through the weekend, during which they are exposed to gap risk. The existence of an around-the-clock trading venue eliminates this constraint at the mechanism level entirely, making it especially attractive to institutions and professional traders that need precise risk management.

If decentralized platforms can continue to expand liquidity and coverage of assets, the market size they can reach would extend from crypto-native trading volume to the global multi-billion-dollar traditional derivatives market. The settlement delays and limited trading hours inherent to traditional markets create a long-term, persistent structural efficiency gap—this is precisely the core entry point for decentralized venues.

Frequently Asked Questions

What is Hyperliquid, and how is it different from centralized exchanges like Binance?

Hyperliquid is a decentralized perpetual futures trading platform that executes order matching directly on-chain. Users’ assets are controlled by smart contracts rather than being custody-held by centralized entities, and the trading records are fully transparent and verifiable. Compared with CEXs like Binance, its liquidity depth and product coverage still have a gap, but it has structural advantages in terms of transparency and asset self-custody.

What practical significance does Hyperliquid’s market share rise from 3.5% to 6% have?

This figure represents Hyperliquid’s share of total trading volume across all perpetual futures platforms (including CEX and DEX). While the overall market’s trading volume declines, its market share grows against the trend, indicating that Hyperliquid is capturing real trading activity from competitors rather than expanding passively by relying on market hype.

What competitive significance does Hyperliquid’s 24/7 trading of commodities like oil have?

Traditional derivatives exchanges such as CME have fixed trading hours. During the weekend when exchanges are closed, investors cannot hedge their positions, facing gap risk. Hyperliquid’s around-the-clock trading mechanism removes this limitation at the mechanism level, giving it structural appeal for institutional traders that require precise risk management, while also building a potential user base that goes far beyond the crypto market.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.