Cryptocurrency Protocols will generate over $16 billion in revenue in 2025, more than double the approximately $8 billion in 2024. Tether and Circle account for 60%, perpetual contract exchanges account for 7-8%, surpassing traditional DeFi. Fees amount to $30.3 billion, retained earnings are $17.6 billion, and token holder returns reach $3.36 billion (accounting for 18%). The three main drivers are interest rate spreads, trade execution, and distribution channels.

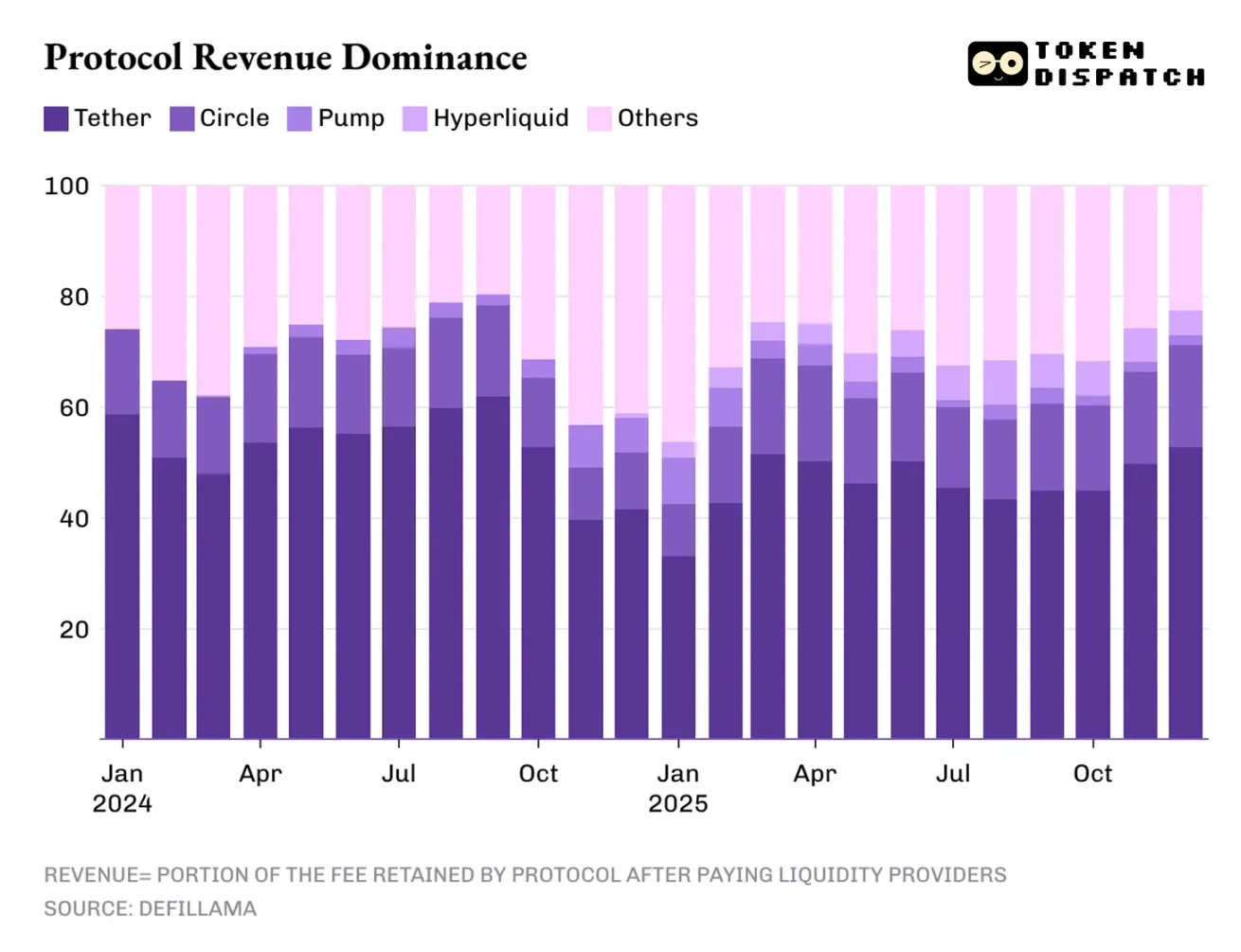

Tether’s 60% Revenue Monopoly and the Threat of Rate Cuts

(Source: Token Dispatch)

Revenue in the cryptocurrency industry is highly concentrated. The top two stablecoin issuers, Tether and Circle, contribute over 60% of the total industry revenue. By 2025, their market share will slightly decline from about 65% in 2024 to 60%. Such concentration is rare in any industry, effectively giving these two companies control over the entire sector.

The revenue model of stablecoin issuers combines structural advantages with vulnerabilities. Structurally, revenue scales with the supply and circulation of stablecoins; each digital dollar issued is backed by U.S. Treasuries earning interest. However, the vulnerability lies in dependence on macroeconomic variables beyond issuers’ control: the Federal Reserve’s interest rates.

When the Fed maintains high interest rates above 5%, Tether’s holdings of U.S. Treasuries generate substantial interest income. Assuming Tether holds $120 billion in reserves invested in short-term Treasuries yielding 5%, annual interest income could reach $6 billion. After operational costs, net profit might exceed $5 billion. This “passive income” business model is highly advantageous in the high-rate environment of 2023 to 2025.

However, with the monetary easing cycle just beginning and rates further decreasing this year, the revenue dominance of stablecoin issuers will weaken accordingly. If the Fed cuts rates to 3%, Tether’s interest income would drop from $6 billion to $3.6 billion—a 40% decline. This revenue compression will force stablecoin issuers to seek new profit models or accept significantly lower profit margins.

The Three Pillars of Revenue in the Cryptocurrency Industry

Interest Rate Spreads (60% revenue): Stablecoin issuers earn interest on U.S. bonds, relying on high interest rate environments.

Trade Execution (7-8% revenue): Perpetual contract exchanges collect high-frequency fees, directly related to trading volume.

Distribution Channels (single-digit revenue): Token issuance platforms like pump.fun charge listing and trading fees.

The fragility of this revenue structure lies in over-reliance on a single model. When Tether and Circle account for 60% of revenue, the overall financial health of the crypto industry essentially depends on the Federal Reserve’s interest rate policy. This unhealthy dependency makes the industry vulnerable to macroeconomic policy shifts.

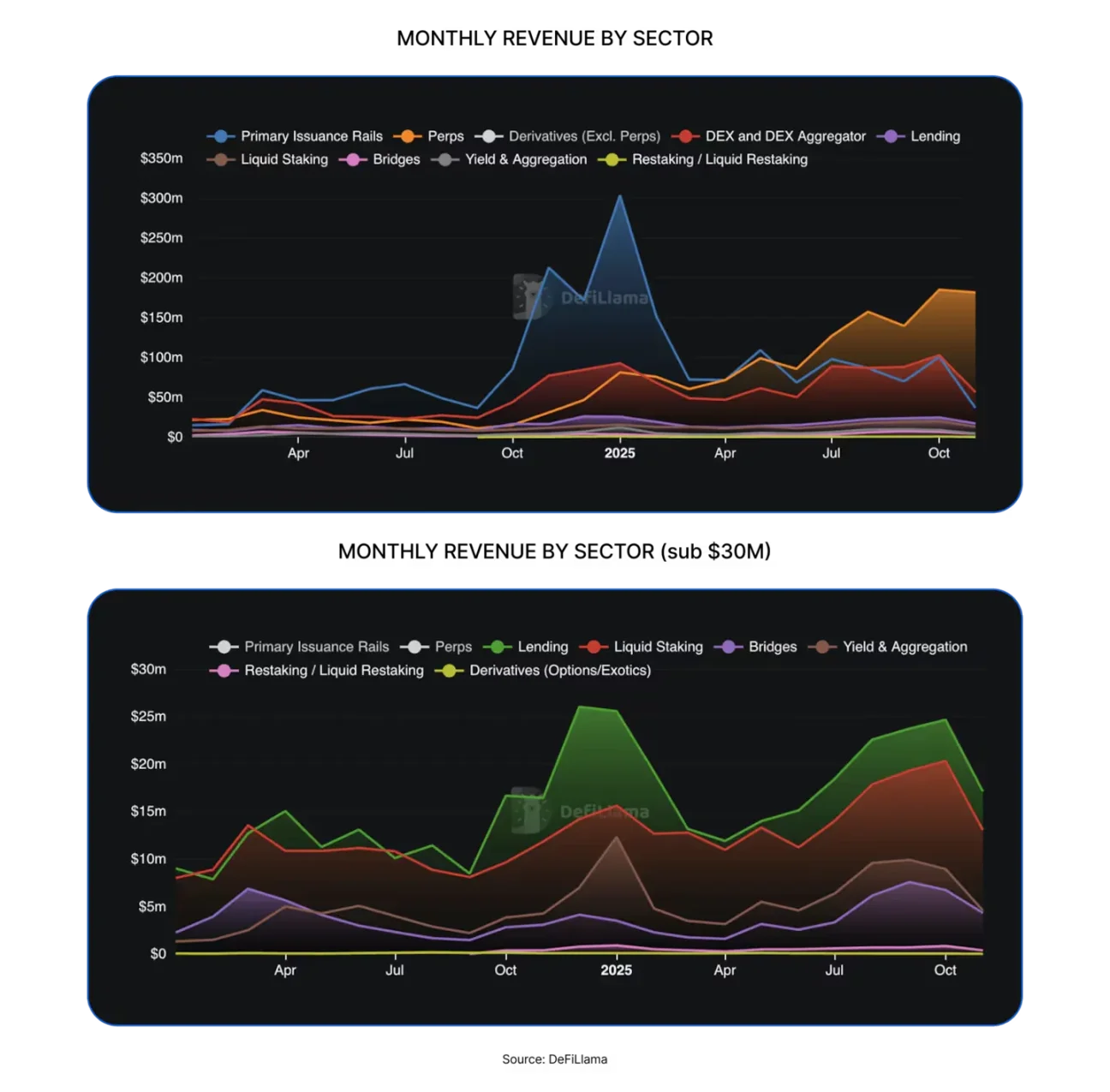

The Explosive Rise of Perpetual Contract Exchanges from 0% to 8%

(Source: DefiLlama)

Decentralized perpetual contract exchanges in 2025 are not to be underestimated; this sector was almost negligible in 2024. Hyperliquid, EdgeX, Lighter, and Axiom together account for 7-8% of total industry revenue, far surpassing the combined protocol revenues of mature DeFi sectors like lending, staking, cross-chain bridges, and decentralized trading aggregators.

The simplest way to understand why decentralized perpetual contract exchanges can quickly capture significant market share is to look at how they help users execute trades. These platforms create a low-friction trading environment, allowing users to enter and exit risk positions on demand. Even in calm markets, users can hedge, leverage, arbitrage, rebalance, or pre-position for future market moves. Unlike spot decentralized exchanges, these platforms enable continuous, high-frequency trading without the hassle of transferring underlying assets.

In 2025, Hyperliquid will dominate the perpetual contract decentralized trading sector by leveraging ample liquidity provided by the largest market makers on its platform. This also led to the platform being the highest fee-earning decentralized perpetual exchange for 10 out of the past 12 months. This sustained leadership confirms the market logic of “liquidity is king.”

Ironically, the success of these DeFi perpetual contract exchanges is due to their avoidance of requiring traders to understand blockchain and smart contracts. Instead, they adopt familiar traditional exchange operations. This “packaging decentralized infrastructure with centralized experience” strategy is key to DeFi mainstream adoption. I believe that although decentralized perpetual contract exchanges only accounted for a small percentage of revenue last year, they are the only sector capable of challenging the stablecoin issuers’ dominance.

$3.36 Billion Rewards and the Paradigm Shift of Value Transfer

In 2025, the total fees paid by users to decentralized finance and other protocols will be about $30.3 billion. Of this, approximately $17.6 billion will be retained by protocols after paying liquidity providers and suppliers. Out of the total revenue, about $3.36 billion will be returned to token holders through staking rewards, fee sharing, token buybacks, and burns. This means 58% of fees are converted into protocol revenue, while only 11% is returned to token holders.

Although this ratio may seem modest, it is a significant shift from previous cycles. More protocols are beginning to treat tokens as ownership claims on operational performance, providing tangible incentives for investors to hold and go long on projects they believe in. Over the past year, the proportion of token holder earnings relative to total protocol revenue has continued to rise, surpassing the previous high of 9.09% early last year, and reaching over 18% at its peak in August 2025.

This change is also reflected in token trading: if my held tokens never generate any returns, my trading decisions are only influenced by media narratives; but if my tokens can generate income through buybacks or fee sharing, I will see them as income-generating assets. Although not necessarily safe or reliable, this shift will influence how markets price tokens, making their valuation more aligned with fundamentals rather than media-driven narratives.

Hyperliquid has built a unique community ecosystem, returning about 90% of revenue to users via the Hyperliquid Assistance Fund. Among token issuance platforms, pump.fun emphasizes “rewarding active platform users,” with daily buybacks that have burned 18.6% of the native token PUMP’s circulating supply. By 2026, “value transfer” is expected to no longer be a niche strategy but a necessary approach for all protocols that want their tokens to trade based on fundamentals.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.