Author: Jasper De Maere

Compiled by: Deep Tide TechFlow

Preface

Liquidity drives the cryptocurrency cycle, but inflows through stablecoins, ETFs, and DATs (Digital Asset Trusts) have noticeably slowed.

Global liquidity remains strong, but higher SOFR (Secured Overnight Financing Rate) is directing funds into government bonds rather than the crypto market.

Currently, cryptocurrencies are in a self-financing phase, with capital cycling internally, waiting for new inflows to return.

Liquidity determines every crypto cycle. While long-term technological applications may be the core driver of the crypto story, it is the movement of funds that truly influences price changes. Over the past few months, the momentum of capital inflows has weakened. In the three main channels through which capital enters the crypto ecosystem—stablecoins, ETFs, and Digital Asset Trusts (DATs)—the flow momentum is diminishing, causing cryptocurrencies to be in a self-financing rather than expansion phase.

Although technological adoption is an important driver, liquidity is the key factor that drives and defines each crypto cycle. It’s not just about market depth but also about the availability of funds themselves. When global money supply expands or real interest rates decline, excess liquidity inevitably seeks risk assets. Historically, especially during the 2021 cycle, cryptocurrencies have been among the biggest beneficiaries.

In previous cycles, liquidity primarily entered the digital asset space through stablecoins, which serve as the core fiat on-ramp. As the industry matures, three major liquidity channels are becoming critical in determining new capital inflows into crypto:

- Digital Asset Trusts (DATs): Tokenized funds and yield structures connecting traditional assets with on-chain liquidity.

- Stablecoins: On-chain representations of fiat liquidity, providing collateral for leverage and trading activities.

- ETFs: Entry points for passive investment and institutional capital exposure to BTC and ETH in traditional finance.

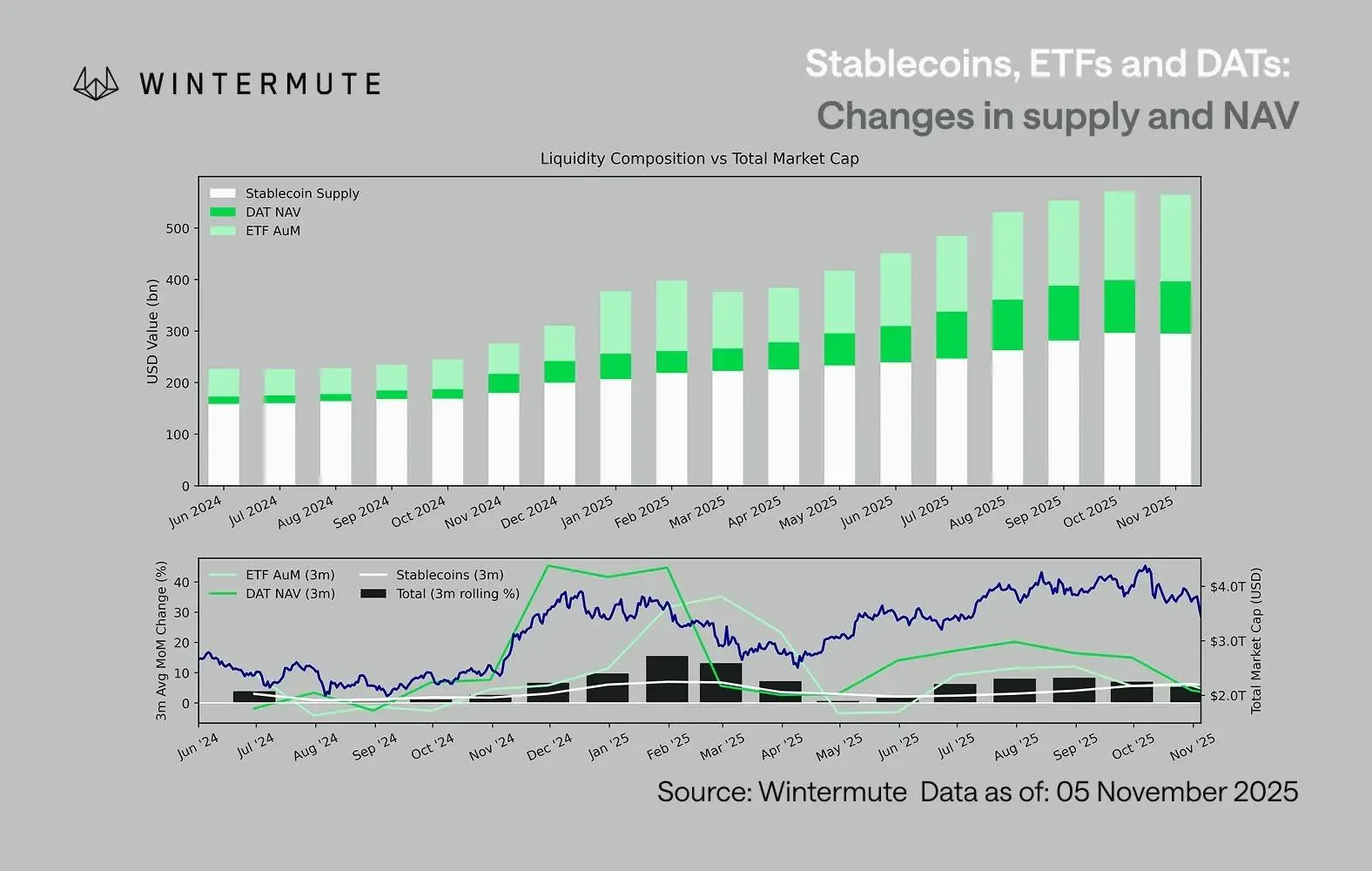

By combining ETF Assets Under Management (AUM), DAT Net Asset Value (NAV), and the number of issued stablecoins, it’s possible to reasonably estimate the total capital flowing into digital assets. The chart below shows the trend of these components over the past 18 months. At the bottom, it’s clear that total volume correlates closely with the overall market cap of digital assets; when inflows accelerate, prices tend to rise.

A key observation is that the inflows into DATs and ETFs have significantly slowed. Both performed strongly in Q4 2024 and Q1 2025, with a brief rebound in early summer, but this momentum has since waned. Liquidity (M2 money supply) is no longer flowing into the crypto ecosystem as naturally as at the start of the year. Since early 2024, the total size of DATs and ETFs has grown from approximately $40 billion to $270 billion, while stablecoin volume has doubled from about $140 billion to roughly $290 billion. Although this indicates strong structural growth, it also shows a clear slowdown.

This deceleration is crucial because each channel reflects different sources of liquidity. Stablecoins represent risk appetite within the crypto industry, DATs capture institutional demand for yields, and ETFs reflect broader traditional financial (TradFi) allocation trends. The simultaneous slowdown across all three suggests a general reduction in new capital deployment, not just a rotation between products. Liquidity isn’t disappearing; it’s merely cycling within the system rather than expanding.

From the broader economy outside crypto, liquidity (M2 money supply) is also not stagnant. Although higher SOFR rates have temporarily constrained liquidity, making cash yields attractive and locking funds into government bonds, the global cycle remains accommodative. The US’s quantitative tightening (QT) has officially ended. The overall structural environment remains supportive; currently, liquidity is being allocated to other risk assets, such as equities.

As external inflows decrease, market dynamics become more insular. Capital is shifting more between mainstream coins and altcoins rather than new net inflows, creating a “player versus player” (PVP) scenario. This explains why market rebounds tend to be short-lived and why market breadth narrows, even as total assets under management (AUM) remain stable. The recent volatility peaks are mainly driven by liquidation cascades rather than sustained trend formation.

Looking ahead, any significant revival in one of the liquidity channels—such as renewed stablecoin issuance, new ETF launches, or increased DAT issuance—would signal macro liquidity flowing back into digital assets. Until then, cryptocurrencies remain in a self-financing phase, with capital cycling internally without generating value expansion.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

Zonda CEO Reveals 4,503 BTC Cold Wallet Inaccessible as Founder Remains Missing Since 2022

Zonda, a Polish cryptocurrency exchange, faces a crisis as its cold wallet containing 4,503 Bitcoin is inaccessible, prompting a surge in withdrawal requests. CEO Kral claims the private key was never transferred during the company's takeover, and authorities are investigating the situation amid bankruptcy fears.

GateNews6m ago

BTC breaks through 75000 USDT

Gate News bot message, Gate market data shows, BTC breaks through 75000 USDT, current price is 75003.9 USDT.

CryptoRadar2h ago

Traditional Brokerage to Launch Spot Bitcoin and Ethereum Trading in Coming Weeks at 0.75% Fee

A traditional brokerage is set to launch spot cryptocurrency trading for retail clients, offering Bitcoin and Ethereum access. The service will include multiple trading platforms, a 0.75% fee, and additional crypto assets planned for the future, reflecting a trend of traditional finance entering the crypto space.

GateNews3h ago

Bhutan Sells $18.46M Bitcoin as Price Nears $74k Resistance

The Royal Government of Bhutan transferred approximately 250 BTC worth $18.46 million in the past 24 hours, according to on-chain data from Arkham, continuing a broader pattern of reduced Bitcoin holdings. The transfers included 162 BTC and 69.7 BTC sent to new wallet addresses within a short

CryptoFrontier3h ago

Bitcoin's BIP-361 Quantum Fix Splits Community Over Address Freezing

A proposed Bitcoin improvement to address quantum vulnerability has divided the cryptocurrency community over whether to freeze legacy addresses, including those attributed to Satoshi Nakamoto. The BIP-361 proposal, which went live on April 14, has sparked debate between prominent figures including

CryptoFrontier4h ago